Reconstitution of a Partnership Firm — Retirement/Death of a Partner

Notes For All Chapters Accountancy Class 12

Topic 1: Introduction and New Profit Sharing Ratio/Gaining Ratio

1. Meaning of Retirement Retirement of a partner means ceasing to be a partner of the firm.

The different ways by which a partner can retire from the firm are:

(i) With the consent of all the partners.

(ii) By giving notice in writing to all other partners of his intention to retire, in case of partnership at will.

(iii) In accordance with the terms of agreement between the partners.

2. Liability of a Partner

Liability of the Firm for the Acts before Retirement [Section 32(2)] A retiring partner remains liable for all the acts of the firm up to the date of his retirement. However, a retiring partner may be discharged from his liability by an agreement between himself, third party and the continuing partners.

Liability of the Firm for the Acts after Retirement [Section 32 (3)] A retiring partner also continues to be liable to third parties for the acts of the firm even after his retirement until a public notice of his retirement is given.

Various matters that need accounting adjustment at the time of retirement are:

(i) Determination of new profit sharing ratio

(ii) Determination of gaining ratio

(iii) Treatment of goodwill

(iv) Revaluation of assets and liabilities

(v) Adjustment of accumulated profits and losses

(vi) Adjustment of capital

(vii) Determination of the amount payable to the retiring partner

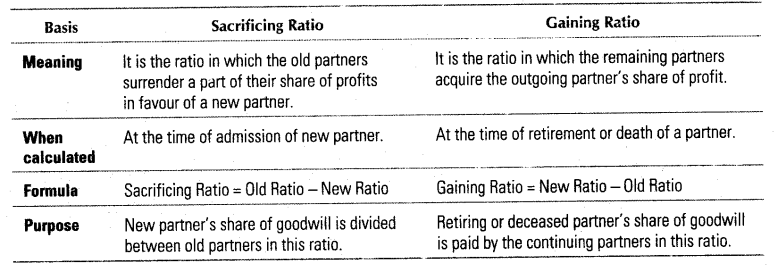

3. New Profit Sharing Ratio The ratio in which the continuing partners will share profits and losses is called new profit sharing ratio. It is the sum total of his old share and the ratio in which the outgoing partner’s share of profit is acquired.

New Ratio = Old Ratio + Gaining Ratio

4. Gaining Ratio The ratio in which the remaining i.e. continuing partners have acquired the share from the retiring partner is called gaining ratio.

Gaining Ratio = New Ratio – Old Ratio

5. Difference between Sacrificing Ratio and Gaining Ratio

Topic 2: Treatment of Goodwill and Revaluation of Assets and Re-assessment of Liabilities

1. Treatment of Goodwill

Goodwill is a compensation paid to an outgoing partner payable by remaining partners in their gaining ratio.

Adjustment for retiring partner’s share of goodwill will be made through the following journal entry

Gaining Partners’ Capital A/c Dr [Continuing partners] [in gaining ratio]

To .Sacrificing Partner’s Capital A/c [Retiring partner]

If goodwill already appears in the old balance sheet, then it is to be written-off in old ratio.

All Partners’ Capital/Current A/c Dr

To Goodwill A/c

2. Revaluation of Assets and Re-assessment of Liabilities

Revaluation of assets and re-assessment of liabilities are to be done in the same way as in the case of admission of a new partner.

3. Adjustment for reserves and accumulated profits/losses Adjustment for reserves and accumulated profits/losses are to be done in the same why as in the case of admission of a partner.

Topic 3: Settlement of Amount Due to Retiring Partner

1. Calculation of Amount Payable to Retiring/Deceased Partner The amount due to a retiring partner is ascertained by preparing retiring partner’s capital account, after taking into account the following

Items to be Credited

(i) Opening balance of capital and current account of retiring partner.

(ii) His share in the profit of revaluation account.

(iii) His share of reserve and accumulated profit.

(iv) His share of goodwill of the firm.

(v) His share of profit till the date of his retirement.

(vi) His salary and/or interest on capital due to the retiring partner till the date of his retirement.

Items to be Debited

(i) Drawings and interest thereon.

(ii) Share in the accumulated losses of past year/years.

(iii) Share in the loss of revaluation account.

2. Settlement of the Amount Due to the Retiring Partner The amount due to retiring partner is either paid off immediately or is transferred to his loan account. The retiring partner’s loan account will appear in the books of the new firm as a liability until it is paid off finally.

Journal Entries

The following journal entries are passed in this regard

(i) If the Amount is Immediately Paid off

Retiring Partner’s Capital A/c Dr

To Cash/ Bank A/c

(ii) In Case the Amount is Not Immediately Paid

(a) For amount due, transferred to retiring partner’s loan account

Retiring Partner’s Capital A/c Dr

To Retiring Partner’s Loan A/c

(b) On interest being provided

Interest on Loan A/c Dr

To Retiring Partner’s Loan A/c

(c) On payment of instalment with interest

Retiring Partner’s Loan A/c Dr

To Cash/Bank A/c

(iii) If Payment is Partly Paid in Cash and the Remaining Amount is to be Treated as Loan

Retiring Partner’s Capital A/c Dr

To Cash/Bank A/c To Retiring Partners’ Loan A/c

Topic 4: Adjustment of Capital

At the time of retirement of a partner, the remaining partners may decide to adjust their capital contributions in their profit sharing ratio.

The capitals of the continuing partners may be required to be adjusted in the following three cases:

Case I When the total capital of the new firm is given

The various steps involved in adjusting the capitals of the partners are given below:

Step 1 Calculate the adjusted old capitals of continuing partners (i.e. after all other adjustments).

Step 2 Calculate the new capitals of continuing partners.

Step 3 Calculate the surplus/deficit capital by comparing step 2 and 3.

Case II When the total capital of the new firm is not given

The various steps involved in adjusting the capitals of the partners are given below:

Step 1 Calculate the adjusted old capitals of continuing partners after all other adjustments.

Step 2 Calculate total capital of the new firm.

Step 3 Calculate the new capitals of continuing partners.

Step 4 Calculate the surplus/deficit capital by comparing step 2 and 3.

Case III When the outgoing partner is to be paid through cash brought by the continuing partners in such a way as to make their capitals proportionate to their new profit sharing ratio

Steps involved in adjusting the capitals of partners are given below:

Step 1 Calculate the adjusted old capitals of continuing partners after all other adjustments.

Step 2 Calculate total capital of the new firm.

Step 3 Calculate the new capital of continuing partners.

Step 4 Calculate the surplus/deficit by comparing step 2 and 3 above.

Topic 5: Death of a Partner

1. Death of A Partner The partnership comes to an end immediately, whenever a partner dies although the firm may continue with the remaining partners.

The deceased partner is entitled to get his share in the firm as per the provision of a partnership agreement. His share in the firm is calculated in the same manner as in the case of a retiring partner.

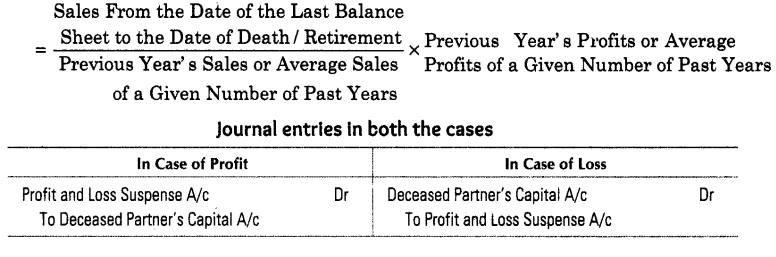

2. Accounting Treatment of Deceased Partners’ Share in Profits If a partner dies on any date after the date of the balance sheet, then his share of profit is calculated from the beginning of the year to the date of death on the basis of time or sales. When share of profit is calculated on the basis of time, it may be on the basis of previous year’s profit or average profit of past years.

On Time Basis

Profit from the date of last balance sheet to the date of death/retirement

Number of Days or Months From the Date of Last

On Sales Basis

Profit from the date of last balance sheet to the date of death/retirement

3. Ascertainment of the Amount Due to the Deceased Partner The deceased partner’s share is also calculated in the same manner as in the case of retiring partner. Amount due to a deceased partner shown by his capital account is transferred to his executors’ account by passing the following journal entry

Deceased Partner’s Capital A/c Dr

To Deceased Partner’s Executors A/c

4. Settlement of Deceased Partners’ Executor Account

(i) If Payment is Made in Full/Lumpsum

Deceased Partner’s Executor’s A/c Dr

To Cash/ Bank A/c

(ii) If Payment is Made in Instalment

(a) Deceased Partner’s Executor’s A/c Dr

To Deceased Partner’s Executor’s Loan A/c

(b) Interest A/c Dr

To Deceased Partner’s Executor’s Loan A/c, Interest is generally paid to deceased partner’s executor’s @ 6% per annum.

(c) Deceased Partner’s Executor’s Loan A/c Dr

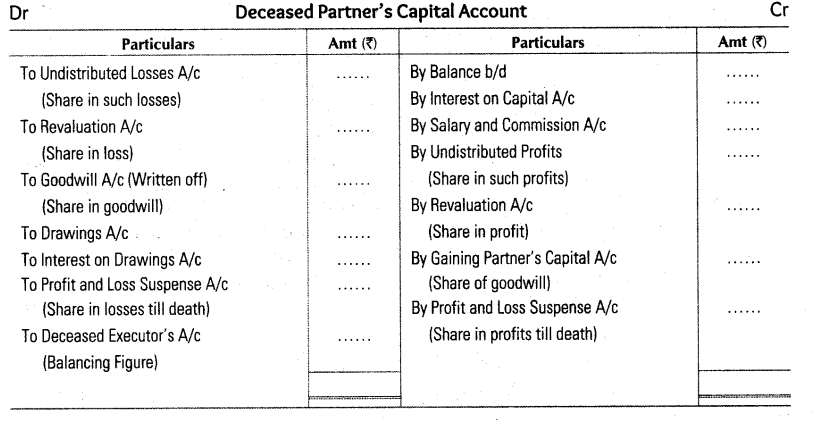

5. Format of Deceased Partner’s Capital Account

Leave a Reply